Most people never see how insurance companies actually operate behind the scenes. The process feels confusing, and that confusion can reduce the value of a claim.

This guide explains the tactics insurers use, how they evaluate injuries, and what strengthens your case.

Insurance adjusters use a structured internal process to decide what your claim is “worth.” It often includes:

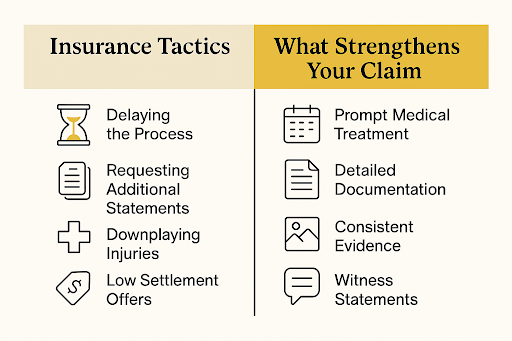

Insurance companies use predictable patterns to control payouts. Understanding them helps you avoid missteps.

The strategy is simple: delay long enough that people accept a lower settlement out of frustration.

Adjusters may ask for broad medical authorizations or repeated interviews.

These are often used to search for unrelated medical history they can point to as an “alternative cause.”

Adjusters sometimes suggest that injuries are “mild,” “preexisting,” or “not supported” by the records—even when medical providers disagree.

Early offers are typically made before the full medical picture is clear.

Insurers know early financial pressure makes quick settlements more likely.

Adjusters may review publicly available photos, videos, or posts.

Short clips or single images are sometimes taken out of context to question the extent of injuries.

Medical documentation is the backbone of a personal injury claim. Insurers look closely at:

• Key terms

Words like “acute,” “radiating pain,” or “loss of function” may carry weight. Missing detail can be used against you.

• Treatment consistency

Gaps in care are often interpreted as “improvement,” even when outside factors, like cost or scheduling, caused the delay.

• Objective findings

Imaging results, physical exam notes, and specialist evaluations help validate reported symptoms.

• Clear diagnosis and prognosis

Insurers prefer records with straightforward assessments. Vague notes can lead to disputes over injury severity.

When insurers want to reduce exposure, they often challenge who is at fault. Common tactics include:

Liability disputes are one of the most common ways insurers reduce claim value.

The same factors insurers scrutinize are the factors that strengthen your case:

These elements help counter many of the tactics insurers rely on.

For example, in car accident claims, complete documentation reduces room for dispute.

In rideshare collisions, trip data and digital records strengthen liability.

In slip and fall cases, incident reporting and photos of unsafe conditions matter.

The same applies to premises liability matters

Some claims reach a point where negotiations stall. This can happen when:

At that point, the options may shift. A lawyer can handle communication, gather additional evidence, or prepare the claim for litigation.

Having counsel changes the process in several ways:

It’s not about being adversarial. It’s about ensuring the claim is evaluated fairly.

If you’re dealing with an insurer and want clarity on the next steps, Echevarria Legal can step in so you don’t get taken advantage of.

You can ask questions, review options, and understand the process before you decide how to move forward.

WhatsApp us for an instant reply